Voluntary redundancy

If you are considering a redundancy offer from British Airways, the infographics and FAQs below will help you to understand your options under NAPS and guide you on where to find information about your NAPS pension.

This page also includes a range of FAQs about leaving under redundancy.

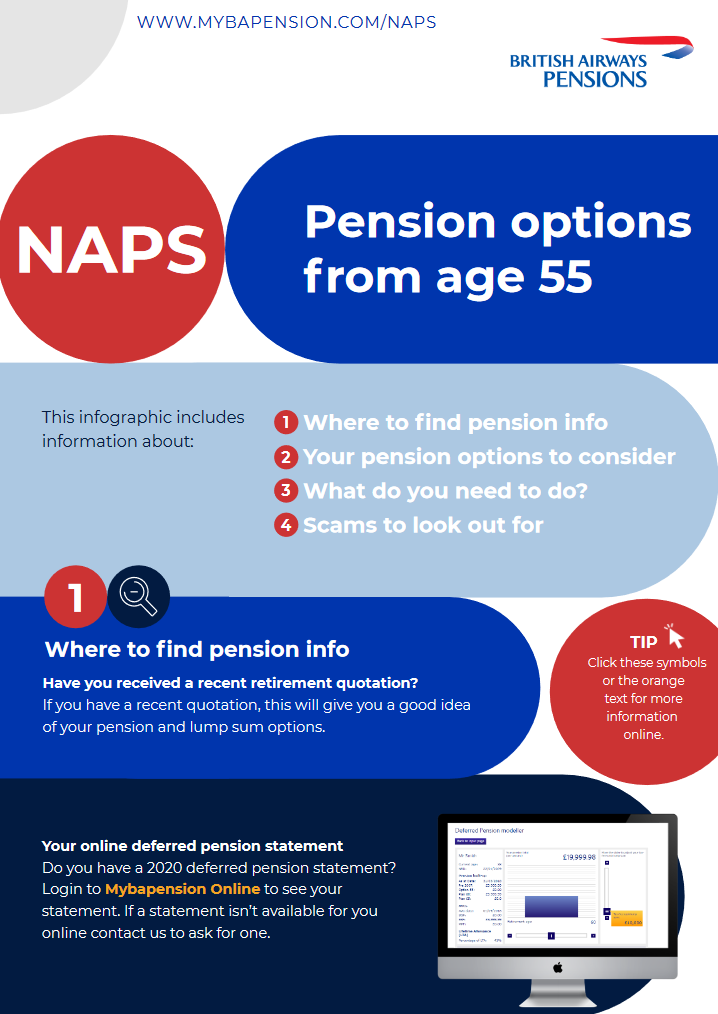

If you have a deferred pension entitlement in NAPS, we provided your latest online yearly statement, as at 6 April 2020, at the beginning of June 2020. Simply login to Mybapension online to view your latest statement.

Your statement shows the current value of your deferred pension and, if you are under age 55, how much pension you will be able to draw from age 55 (the earliest retirement age under NAPS).

Pension modeller

You can also use the online pension modeller to view your tax-free lump sum and pension options at different retirement ages (up to age 65). Your tax-free lump sum automatically includes your AVCs, if you have a NAPS AVC account.

Your latest AVC fund balance

If you have a NAPS AVC fund, you can view your latest available AVC fund balances by clicking on the ‘Smart Additional Voluntary Contributions (SmartAVCs)’ link under ‘Your e-Forms’.

CloseBA introduced BAPP for its existing employees from 1 April 2018. Contact Aviva Life & Pensions on 0345 030 7964 or log into your BAPP account via the BA intranet for details of your BAPP account value and options.

CloseYes, you can. From your NAPS pension, you can generally take up to 25% of the value of your total Scheme benefits on the date you start to draw them. If you also have a British Airways Pension Plan (BAPP) account with Aviva, you may also be able to take up to 25% of your account as a tax-free lump sum. The overall maximum lump sum you can take from all pension arrangements you belong to is 25% of your available lifetime allowance.

How to work out the value of your NAPS pension

The value of your NAPS pension is worked out as 20 times your annual rate of pension. So, if your NAPS pension is £6,000 a year and you do not take a tax-free lump sum when you start to receive your pension, the value of your pension is worked out as follows:

20 x £6,000 a year = £120,000

Or, if you take a tax-free lump sum, the value of your pension is worked out as 20 times your remaining yearly pension, plus the value of your lump sum:

20 x £4,200 a year = £84,000 plus your lump sum of £20,000 = £104,000

If you usually receive yearly deferred pension statements, you can login to Mybapension online to view your latest statement. You can also use the NAPS deferred pension modeller to understand your pension and tax-free lump sum options. If you have any further questions about your NAPS pension, please contact us through our online contact us form.

CloseYou can leave any remaining AVCs invested in NAPS and use them to buy pension benefits later, or you can transfer them to another pension arrangement (including to BAPP). BA Pensions does not endorse a transfer to BAPP over any other provider.

CloseCan I take my pension?

You can take your NAPS benefits at any time from age 55 if you wish. If you draw your pension earlier than your normal retirement age (NRA), your pension payments will be reduced to allow for the longer payment period.

Can I draw my AVCs only first?

There is no option under NAPS to take a tax-free lump sum or draw only your AVCs separately from your NAPS pension. However, you can transfer some or all of your NAPS AVCs independently of your NAPS deferred pension to another approved pension arrangement.

CloseWe have detailed information about finding regulated retirement advice on the ‘Financial advice’ page of this website, including where to find an adviser and a useful guide from the Financial Conduct Authority on ‘What to ask an adviser’. The ‘Financial advice’ page also includes details of our Pension Advice Allowance option, which allows you to use up to £500 of your NAPS AVCs towards regulated retirement advice.

CloseIf you were a member of NAPS on 31 March 2018, you would have been entitled to a deferred pension entitlement in NAPS. This is due to be paid from your normal retirement age (NRA) (which is age 55 for any pension earned under Option 55, age 60 for pension earned under Plan 60 or 65 for pension earned under Plan 65). If your NAPS membership began before 31 March 2007, you would be entitled to a pension for pre-2007 service and a pension for post-2007 service. These may have different NRA's; however, they must be treated as a single pension entitlement and drawn at the same time.

When you are approaching your NRA (in NAPS, this will be the NRA that applied on the date your active membership of the Scheme ended), we will write to you with full details of your NAPS pension benefits and options about four months beforehand.

You can contact us to ask for a retirement quotation at any time. Where possible, please allow at least four months between the date of your request and the date you wish to draw your NAPS pension.

CloseIf you are over age 55, you can usually draw your pension immediately. If you are under your normal retirement age (NRA), and you have registered to manage your pension online, you can use the deferred pension modeller to model your pension and lump sum options at different retirement ages.

You can contact us to ask for a retirement quotation at any time. Where possible, please allow at least four months between the date of your request and the date you wish to draw your NAPS pension.

CloseNo. NAPS closed to future build up after 31 March 2018. You will be able to pay a redundancy payment into your BAPP or SIPP pension. Contact Aviva Life & Pensions on 0345 030 7964 for further information.

CloseIf you are considering retiring within the next four months, please contact us to request a retirement pack. Please bear in mind that our response times are likely to be longer than usual during the Coronavirus outbreak. If you are under your normal retirement age (NRA) and you have registered to manage your pension online, you can use the deferred pension modeller to model your pension and lump sum options at different retirement ages.

CloseNo. The Scheme does not currently include flexible retirement options. If you have NAPS AVCs, you can choose to transfer them independently of your NAPS deferred pension. You can choose to transfer just your AVCs out of the Scheme, or you may choose to transfer your main Scheme pension out as well. Before transferring benefits out of the Scheme, you should get free guidance from Pension Wise (www.pensionwise.gov.uk) to make sure any new arrangements meet your needs and that you fully understand how this will affect any tax you have to pay.

CloseA pension transfer from a defined benefit (DB) pension scheme such as NAPS means giving up your benefits in the Scheme (and any dependants’ benefits you have paid towards) in return for a cash value which is invested in another pension scheme of your choice. Vist the Can I transfer my pension out? page to learn more about this option.

CloseYou can take a partial transfer out of your NAPS pension and leave the rest within the Scheme if you have a deferred pension entitlement which was built up over two or more specified periods.

NAPS pensions are generally made up of three main portions, built up over the following periods:

- Pension earned before April 1997*

- Pension earned between April 1997 and April 2007

- Pension earned after April 2007

A NAPS member who has a deferred pension which was built up during two or more of these periods has one opportunity to make a partial transfer out before drawing or transferring out their remaining Scheme benefits at a later date.

* In all cases, any pension earned before April 1997 must be included in a partial transfer out.

Visit our Partial transfers page for more information about this option.

ClosePlease use the online ‘Contact us’ form to request a CETV quotation, or call us on 020 8538 2100 (9am to 1pm, Monday to Friday).

Close